If there was ever a time to throw out the word “bifurcation” in casual conversation, this is it. Houston’s office market has told two compelling, yet starkly different stories over the last few years – one of high vacancies and tenant friendly deal terms as landlords struggle to stay in the game; another of strong competition, rapid absorption and unprecedented rental rates.

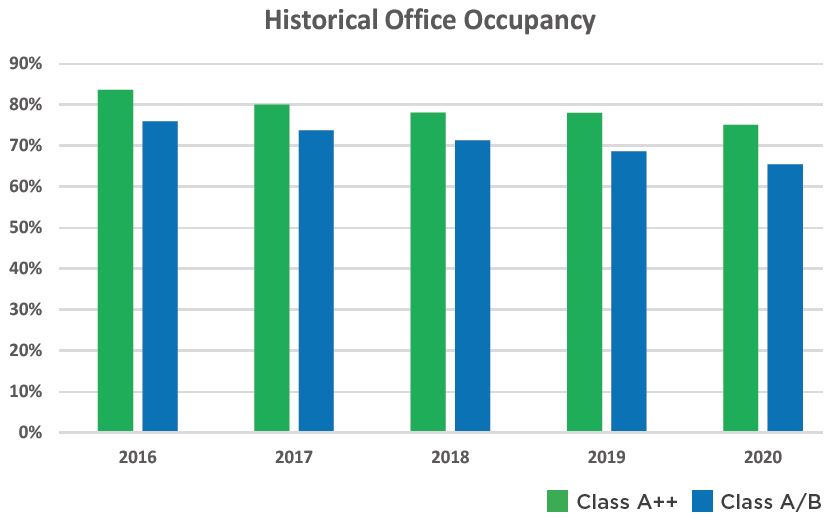

Focusing on the latter, a “flight to quality” among tenants has been trending as new trophy buildings continue to fill up first despite more than 22% overall availability in the Houston market – a stat that placed Houston dead last in terms of occupancy out of the 390 US office markets to close out 2020. The surplus of economical options currently available to tenants makes it even more remarkable that healthy demand for high-quality, high-priced space continues to prevail.

Houston’s Downtown market currently has 1.3 million SF of high-end office under construction, which will further saturate an already struggling market with additional supply. The CBD hasn’t seen these levels of vacancy since the 1980s. However, developers like Hines and Skanska, both of which have trophy projects currently underway in the submarket, remain unwavering given the facts.

So, what are the facts?

Since 2011, more than 8.6 million SF of new Class A+ space has been delivered to Houston’s office markets and today this space is 16.6% vacant, notably lower than Houston’s citywide vacancy of 22.5%. Roughly half of this new space inventory was delivered in Downtown Houston, and this 4.1 million SF is currently less than 6.5% vacant. Compare this to Downtown’s 22.1% overall vacancy, and it becomes clear why the Class A+ construction pipeline has kept pace despite downside risk in the overall market – tenants are continuing to seek out new high-end space even when presented with an array of less expensive options

Throughout the Houston metro, more than 100 buildings currently have 100,000+ SF of contiguous office space available, according to CoStar. Meanwhile, there is more than 3.2 million SF of Class A++ space in the early stages of development across Houston. Landlords of older inventory fight to stay competitive, forced to dig deep into their pockets to fund building updates and large-scale capital improvement projects as they attempt to level the playing field.

Prior to the pandemic, employers decided top-notch, trendy office space was a key contributor toward attracting and retaining the top talent among the younger workforce. The luster of these trophy properties better aligned with some tenants’ long-term business objectives, regardless of the high price tag. Now, it remains unclear exactly how the work from home movement will affect tenants and their office space needs. Even if the office itself takes on a less critical role to a company’s operations, quality and amenities have proven to be more critical than ever.